Interest rate trends over the last 5 years:

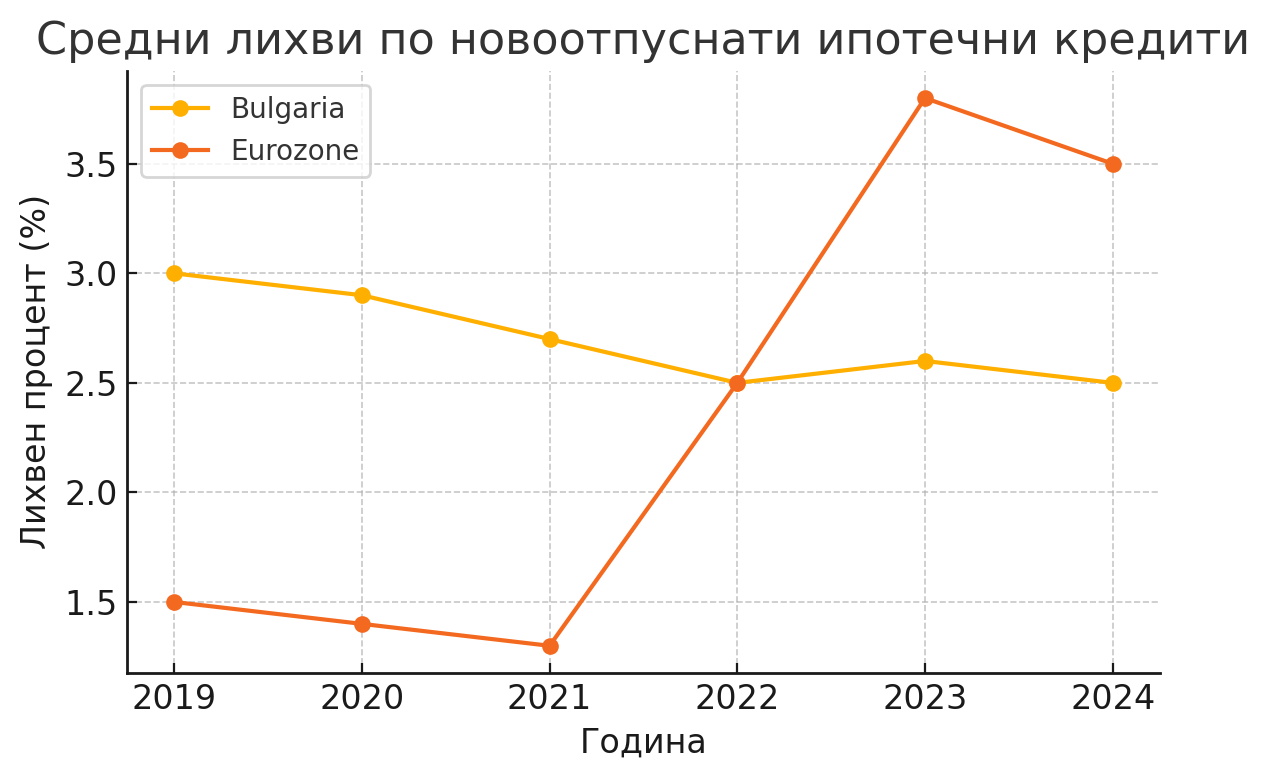

During the period 2019–2024, interest rates on newly granted housing loans in Bulgaria recorded a significantly more moderate movement compared to those in the Eurozone. At the beginning of the period, average mortgage rates in our country were around 3% – for example, at the end of 2018, the average interest rate on a new lev housing loan was 3.24%, and in 2019 it decreased to around 3.0%. In the following years, the trend is downward: at the beginning of 2020, the average interest rate on housing loans in levs fell to 2.97%. These decreases continued in 2021, with interest rates reaching historically low levels. In fact, 2022 will go down in history as the year of record low mortgage interest rates in Bulgaria – in the summer of 2022, the average interest rate on new housing loans reached a bottom of around 2.4% per year. For example, in September 2022, the average effective annual interest rate on housing loans in our country decreased to 2.46% - an unprecedented low in recent credit history.

Since the fall of 2022, there has been a slight increase, but it is minimal. Unlike other countries, Bulgarian banks did not undertake a sharp increase in interest rates in 2023. At the end of 2023, the average interest rate on newly granted mortgage loans was around 2.5–2.6%, which is only slightly above the record lows. According to data from the Bulgarian National Bank (BNB), in September 2023 the average interest rate on new housing loans in levs was 2.61%, compared to 2.47% a year earlier (September 2022). Even until the end of 2024, interest rates remained close to these low values – in November 2024 the average interest rate was 2.51%, even lower than November 2023 (when it was 2.58%). This means that in the midst of a global interest rate hike cycle, Bulgarian mortgages continue to be granted at the lowest interest rates in the European Union (after Malta). For comparison, even when all fees and commissions are included, the average Annual Percentage Rate (APR) on housing loans in Bulgaria in November 2024 was 2.82%, or below 3% – a level that remained virtually unchanged from a year earlier.

Chart: Average interest rates on new mortgage loans in Bulgaria and the Eurozone (2019–2024). Bulgarian interest rates (yellow line) are decreasing and holding around 2.5%, while average interest rates in the Eurozone (orange line) are increasing sharply after 2021.

Factors affecting interest rates in Bulgaria: The low interest rates on mortgage loans in Bulgaria in recent years are due to several key factors. First, the monetary policy and the financial system - Bulgaria has a currency board and a fixed lev/euro exchange rate, which limits the direct interest rate interventions of the BNB. The key interest rate (KIR) announced by the BNB remained 0.00% in the period 2018–2021 and began to rise only at the end of 2022 after interest rate increases in the euro area. This means that domestic monetary policy did not put pressure on interest rates on loans. However, the BNB took other macroprudential measures to cool the credit boom - it gradually increased the countercyclical capital buffer for banks and introduced stricter requirements for mortgage lending. From October 2024. The regulator has required banks to grant housing loans only under certain conditions: a maximum loan-to-value ratio of 85%, monthly payments not to exceed 50% of the client's income, and a loan term of up to 30 years. These steps are intended to limit risky lending without directly increasing the cost of loans.

Second, the excess liquidity of the banking system has contributed to cheap lending. Over the past decade, household deposits have grown significantly, while savings rates have remained close to zero. As of August 2024, the average interest rate paid by banks on funds borrowed from companies and individuals is only 0.11% – practically at no cost to banks. As a result, banks have excess liquidity and can afford to lend aggressively at low interest rates, while maintaining high profit margins. Competition to attract new borrowers further stimulates banks to keep interest rates on new mortgage loans as low as possible. In fact, the BNB statistics only take into account interest rates on newly granted loans, namely for new customers, banks offer the most favorable conditions, while on loans already granted, a slow “creeping” increase has recently been observed.

Third, the economic environment and inflation in Bulgaria also have an impact. In the years before the pandemic and during COVID-19, interest rates gradually fell against the backdrop of low inflation and stable growth. However, in 2022, Bulgaria, like the rest of the world, was hit by a sharp spike in inflation – consumer prices in our country rose by over 15% during the year. Traditionally, high inflation should also lead to higher interest rates, but in this case, banks chose to absorb part of the inflationary blow by keeping lending rates low. This can be explained by their desire to increase their market share in the mortgage lending segment, as well as by expectations that inflation will be temporary. Indeed, in 2023, inflation in Bulgaria began to decline (annual inflation as of December 2024 is only 2.2%), which probably makes it easier to maintain low interest rates. Moreover, the labor market remained extremely strong – unemployment is at historic lows and wages are growing at double-digit rates. Secure income and high employment give banks confidence in the solvency of customers and allow for more relaxed lending at low interest margins, without a significant increase in credit risk.

Fourth, the rapid demand for properties and the growth in their prices in recent years have created the prerequisites for an accelerated growth in housing lending. Many households rushed to buy a home, taking advantage of the low monthly mortgage payments and the fears that high inflation would “eat up” their savings if they did not invest them in real estate. This has given rise to a real credit boom – banks are granting record volumes of housing loans. In the period January–November 2024 alone, new mortgages for BGN 7.2 billion were granted (excluding refinancing) – a growth of 44% compared to the same period in 2023. On an annual basis, the growth rates of the mortgage portfolio are consistently double-digit – for example, in November 2023, newly granted housing loans were 22.5% more than in November 2022. This credit boom has further motivated banks not to raise interest rates, so as not to lose momentum in the market. Experts warn that too easy access to cheap loans inflates property prices and potentially leads to imbalances. The BNB has officially expressed concern about the accumulation of medium-term risks - households are increasing their indebtedness and may encounter difficulties if contributions rise significantly in the future. For now, however, the banking sector is well-capitalized and profitable, which allows it to take on greater credit risk.

Forecasts for the period 2025–2026 in Bulgaria: The prospects are for a gradual and moderate increase in mortgage interest rates, but not for sharp jumps. At the beginning of 2025, there are no indications that Bulgarian banks will increase rates - competition for customers remains strong and they continue to offer loans on favorable terms. Analysts expect that possible increases will occur later in the year and will be in small steps. For example, a bank manager's forecast indicates that in 2024 two increases in interest rates are possible - by about 0.15–0.20 percentage points at the beginning of the year and another ~0.20 percentage points in July. This suggests that even by the end of 2025 the average interest rate may remain around or slightly above 3% - still a low level in historical terms.

An important factor for future interest rates will be the adoption of the euro. If Bulgaria advances towards membership in the eurozone (possibly in 2025–2026), banks may preemptively adjust the price of loans. The reason is that with entry into the eurozone, conditions will gradually level out with other countries – including interest rates that would rise to average European levels. Experts point out that the prospect of the euro is among the factors that would prompt banks to raise interest rates, albeit gradually. Also, if the BNB decides to further tighten credit expansion (for example, to lower the debt/income ceiling from 50% to 45% or to increase reserves), this could indirectly make mortgage loans more expensive.

Overall, the forecast is for a moderate increase: probably in 2025, mortgage interest rates will increase by a few tenths of a percent, but will remain below those in the eurozone. There are even scenarios in which banks will maintain current levels until the euro is introduced, especially if inflation falls to the target of 2% and the European Central Bank (ECB) begins to reduce key interest rates. Some analysts believe that a more tangible increase in interest rates is possible only in the second half of 2026, and then if the economic situation requires it. In any case, the levels will remain competitive and relatively low for our market, as banks will continue to fight for customers and balance profitability for shareholders and affordability for borrowers.

Interest rates in the European Union: policies, crises and comparisons

ECB policy and inflationary pressures: In recent years, the interest rate picture in the European Union (and especially in the euro area) has been dominated by the dramatic policy reversal of the European Central Bank. In the period 2019–2021, the ECB maintained record low key interest rates, even negative on deposits, in an attempt to stimulate lending and the economy. This also led to historically low mortgage rates in most countries – by the end of 2021, the average interest rate on new housing loans in the euro area was just 1.32%. Everything changed in 2022, when a sharp rise in inflation (provoked by the energy crisis, the recovery from the pandemic and the war in Ukraine) forced the ECB to tighten monetary policy. Since spring 2022, the central bank has launched the fastest rate hike cycle in its history – key interest rates were increased from 0% to 4% in just about a year and a half. This change was directly reflected in the credit market: average mortgage rates in the eurozone jumped from around 1.3% at the end of 2021 to nearly 4% in the second half of 2023. Specifically, the average interest rate on new home loans in the eurozone rose to 3.88% as of August 2023, compared to 2.20% a year earlier (August 2022). This three-fold jump in a short period of time set a record and surpassed the rate of appreciation observed even before the Great Financial Crisis.

The sharp increase in interest rates has had a chilling effect on housing markets in many countries. On the one hand, monthly payments on new loans have increased significantly, making housing less affordable for buyers. On the other hand, banks have tightened lending standards – as they expect higher interest rates to make it more difficult to service loans, financial institutions have become more cautious. As a result, the volume of new mortgage loans has fallen, and in several EU countries the net flow of housing loans has even turned negative in 2023 (repayments exceed new loans). The trend is particularly strong in countries where floating mortgage rates prevail and households are heavily indebted – for example, Sweden, where due to massively variable interest rates, annual household interest costs jumped from 1.5% to 6.8% of their income in 2022. In general, the effect of more expensive credit in the EU is manifested in a slowdown in property markets: in many countries, housing prices stopped growing or started to fall after 2022, especially where there was previously "overheating" (Germany, the Netherlands, the Czech Republic, etc.).

Energy crisis, geopolitical instability and their impact: The energy crisis of 2021–2022, triggered by the sharp increase in gas and oil prices, played a decisive role in accelerating inflation in Europe. Increased electricity and fuel prices were transmitted throughout the economy, raising costs for households and businesses. Annual inflation in the euro area peaked at over 10% in October 2022 – the highest level in the history of the euro. This price shock forced the ECB to respond by tightening monetary policy, which – as we have indicated – led to a surge in interest rates. Geopolitical instability also contributed: the war in Ukraine disrupted energy supplies in Europe, increased uncertainty and sharpened inflation expectations. Investors began to demand higher bond yields, which also affected benchmark interest rates in the economy. The banking sector is calculating a larger risk margin in loan interest rates, given the increased geopolitical and economic uncertainty.

In addition, central banks outside the eurozone have taken even more drastic action. In countries such as Poland, the Czech Republic, Hungary, and Romania – which were hit by double-digit inflation – key interest rates were raised to very high levels (e.g., the Polish central bank raised its interest rate to 6.75%, and the Hungarian central bank to over 13% in 2022). This also affected mortgage rates there, and in some cases the increase was even more dramatic than in the Eurozone. For example, at the end of 2023, average mortgage rates reached around 7–8% in Poland, 6.5% in Hungary, while in countries such as Germany, France, and Italy they remained in the 3–4% range. This highlights the influence of national policies and risk premia – where inflation was higher and the exchange rate was weaker, mortgages became more expensive.

Comparison across EU countries: The picture of mortgage interest rates in Europe at the beginning of 2025 shows significant differences (Table 1). The table shows the average interest rates on new home loans in several selected EU countries:

Country Average mortgage interest rate

(early 2025)

| No. | Country | Percentage | Note |

|---|---|---|---|

| 1 | Malta | 1.7% | lowest in the EU |

| 2 | Bulgaria | 2.8% | second lowest |

| 3 | Spain | 2.9% | |

| 4 | France | 3.1% | |

| 5 | Italy | 3.1% | |

| 6 | Germany | 3.5% | |

| 7 | Hungary | 6.6% | |

| 8 | Poland | 7.8% |

Table 1: Comparative interest rates on housing loans in selected EU countries (percentage per annum).**

*Source: data from central banks, summarized in GlobalPropertyGuide.

It is clear that eurozone countries such as Malta, France, Italy, Spain, Germany have average interest rates between ~3% and 3.5%. This largely reflects the ECB’s single monetary policy – they all experienced a similar percentage jump from around 1% to 3–4% over the last two years. At the same time, Bulgaria continues to stand out with lower interest rates (~2.8%), despite not being a member of the eurozone – an effect of our specific domestic conditions discussed above. Malta is a special case with the cheapest mortgages (~1.7%), which is due to a combination of factors such as a high share of fixed rates, state subsidies and a slower transmission of ECB decisions to the local market. On the other side of the spectrum are some Eastern European countries outside the eurozone – Poland and Hungary – where the fight against inflation has led to much higher interest rates (6–8%). Their mortgage markets literally “froze”: in Poland, for example, new mortgage lending collapsed after interest rates jumped above 7%, and many households experienced difficulties with their floating old loans.

Future expectations (EU, 2025–2026): At the beginning of 2025, the main question is whether interest rates in Europe have peaked. Most analyses suggest that the peak is near or has already passed. Eurozone inflation is gradually slowing (ECB projections are for an average of 2.0% in 2025 and 1.6% in 2026), which would allow the ECB to stop raising interest rates and even consider cuts. Market expectations are that key interest rates will stabilize in the second half of 2024, and a gradual decline may begin in 2025 – it is predicted that the ECB deposit rate may return to 2–3% by the end of 2025 (from 4% currently). If these forecasts come true, mortgage rates in the eurozone will also gradually decline. There are already slight indications of this: for example, in Ireland the average interest rate on new mortgage contracts at the end of March 2025 was 3.77%, slightly lower than in previous months. A similar trend – of smooth stabilization and minimal decline – can be observed in other countries with a high jump in 2022–2023.

However, it should be noted that the time lag effect may keep lending rates high even after the ECB changes course. Many of the loans already granted have a fixed interest rate for the first 5–10 years, so the average levels of new deals will more likely reflect the increases already implemented. In other words, even if the ECB starts cutting key rates in 2025, mortgage rates will fall slowly – banks will wait for confirmation that inflation is under control and will assess the risks. The scenario for a decline could accelerate if the European economy falls into a deeper slowdown or recession – then the central bank would cut rates aggressively and lenders would follow. But at the moment, the baseline scenario is for a smooth stabilization: interest rates to remain around the levels reached in 2024 and possibly fall by 0.5–1 percentage point. by the end of 2026. This would leave the average interest rate on housing loans in the eurozone somewhere around 3% after two years – still higher than the extremely low levels of 2020, but far below the peak of almost 4% in 2023.

Uncertainties and risks to the outlook: Despite the relatively optimistic outlook (that the worst is behind us), significant uncertainties remain. A new geopolitical shock – for example, an escalation of war or other international conflicts – could shake up energy markets again and revive inflation, forcing the ECB to keep interest rates high for longer. Also, if inflation turns out to be more persistent (for example, core inflation excluding energy remains above target), central bankers could delay or cancel planned cuts. Separately, differences between countries will continue – southern countries with traditionally lower interest rates (such as Malta, Portugal) are likely to maintain their advantage, while countries with chronically higher inflation (such as Hungary, Poland) may not be able to quickly lower their lending rates.

European interest rate policy is entering a new phase of normalization after the shocks of 2022–2023. For real estate professionals, this means planning for a moderately higher interest rate environment, without relying any longer on the near-zero rates of the past decade. However, by historical standards, the expected levels of ~3% for the euro area and ~3% for Bulgaria will still be favorable and manageable. It will be crucial for the market guardians – the central banks – to successfully tame inflation without causing new shocks, so that the interest rate horizon remains predictable and sustainable.

Register for free to be the first to hear the news on imi.bg

Register